After making a Low of 5:755% in June 2020 the 10 Years GSec Bond Yield is at 6:20%......

What I presume is that it is a Bounce back......but there are No Uptrend Visible of Bull Market in 10 Years GSec Bond Yield.......

After making a Low of 5:755% in June 2020 the 10 Years GSec Bond Yield is at 6:20%......

What I presume is that it is a Bounce back......but there are No Uptrend Visible of Bull Market in 10 Years GSec Bond Yield.......

Power Finance Corporation (PFC) is raising Rs 5,000 crore by issuing non-convertible debentures (NCDs). Coming from a public sector enterprise, it is being seen as an opportunity by many fixed income investors for investing, especially given the current low-yield environment. But is it really worth invest in the issue?

What’s on offer

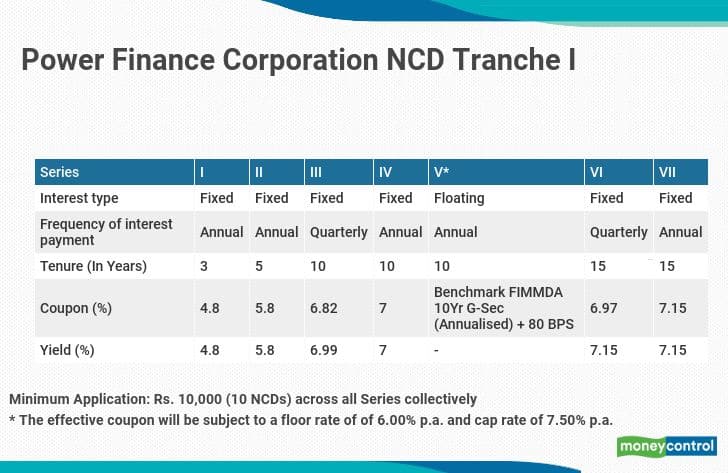

PFCplans to issue secured, redeemable NCDs in dematerialized form on a first-come first-serve basis. The issue opens on January 15, 2020. Three credit rating agencies – CRISIL, ICRA and CARE – have given AAA rating to this issue. The minimum application size is 10 NCDs, aggregating to Rs 10,000 collectively across all series of NCDs and in multiples of One NCD of face value of Rs 1000 each thereafter.

PFC is a non-banking financial institution engaged in the business of extending loans to the power sector.

There are seven different options that PFC offers in the proposed NCD issue. Three and five-year bonds offer annual payouts of interest at the rate of 4.8 percent and 5.8 percent, respectively. On 10-year bonds, you have the option of choosing quarterly or yearly payout with coupons of 6.82 and 7 percent, respectively. You also have the option of floating-rate 10-year bonds that pay 80 basis points more than the Benchmark FIMMDA 10-Year G-Sec (annualized) – subject to a minimum of 6 percent and a maximum of 7.5 percent. In the 15-year tenure, you have two options to receive coupons at the rate of 6.97 and 7.15 percent for quarterly and yearly periods, respectively.

The NCD will be listed on the BSE. There is no put or call option attached to these NCD. The issue closes on January 29, 2021.

What works

The issuer is a central public sector enterprise and has the highest credit rating from three agencies. This indicates least credit risk. The listing on the stock exchange would allow investors to exit before maturity if they need to. Vikram Dalal, Founder & Managing Director of Mumbai based Synergee Capital Services says, “Since this is a large issue of Rs 5000 crore, the bonds are more likely to see good liquidity on the stock exchanges.”

Tax will not be deducted at source on interest paid.

“Comparable 10-year AAA-rated PSU bonds are quoting in the range of 6.5 to 6.6 percent. As this bond offers 7 percent, there is a potential for listing gains,” says Deepak Panjwani, Head-Debt Markets, GEPL Capital.

What doesn’t

The interest paid on these bonds are taxable in the hands of investors. Hence, individual investors in the higher tax slabs may not find it attractive.

The rates offered are low. For example, the three-year NCD offers 4.8 percent. This is way below the 5.3 percent rate of interest offered by SBI on its three-year fixed deposits. Same is the case with the five-year NCD variant that offers 5.8 percent. The five-year National Saving Certificate pays interest at the rate of 6.8 percent compounded annually at the time of maturity.

That leaves you with long term choices maturing in 10 and 15 years, which may not be suitable for many investors given their liquidity needs.

The effective yield offered by the company is 9.09-9.70%. In comparison, NCDs by some of the other non-banking financial companies such as LIC Housing Finance, ICICI Home Finance and HDFC are offering interest in the range of 5% to 6%

Edelweiss Financial Services Ltd on Thursday will launch a secured non-convertible debenture (NCD) issue of up to ₹400 crore, offering an effective yield of up to 9.70%. The issue will close on 23 April. The issue has a base size of ₹200 crore with a greenshoe option to retain oversubscription of up to ₹200 crore.

In the draft prospectus, the company said it operates in a highly competitive market and faces significant competition from other players.

“Many of our competitors are large institutions, which may have a larger customer base, funding sources, branch networks and capital base compared to us. Some of them may be more flexible and better positioned to take advantage of market opportunities. This competition is likely to further intensify as a result of liberalization and regulatory changes," Edelweiss said.

While the issue is secured, the security is against the future cash receivables of the company. According to the firm, the funds raised will be used for repayment or prepayment of interest and principal of existing borrowings as well as general corporate purposes.

The issue offers up to 9.70% yield for a tenor of 120 months and the issue has been rated AA with negative outlook by Acuité Ratings & Research and AA- with stable outlook by Brickwork Ratings. These ratings mean that the debentures carry low credit risk but are not as safe as AAA-rated instruments, while a negative outlook means that a rating may be lowered in the future.

The issue comes with three tenors (36, 60 and 120 months) and three options for interest payment frequency (annual, monthly and cumulative).

The effective yield offered by the company is in the range of 9.09% to 9.70%. In comparison, NCDs by non-banking financial companies such as LIC Housing Finance, ICICI Home Finance and HDFC are offering interest in the range of 5% to 6%. Experts say that an NCD issue offering higher returns will have a high

“The higher the returns, the more risk the issue will have. Investors in a fixed income must realize that anything below an AA rating comes with credit risk. Even as the rating is AA for the Edelweiss issue, the rating agencies are not among the bigger names. Moreover, one of the rating agencies has a negative outlook on the issue. This issue is only meant for people who understand the risks of investing in a credit paper, and even if they are investing, they should only go for the lowest tenor, which is 36 months," said Kirtan Shah, chief financial planner at Sykes and Ray Equities (I) Ltd.

Investors must note that redeeming NCDs before maturity might be a challenge, as the Indian debt market is not that deep. They must also be mindful of taxation, as interest earned on these NCDs is taxed at the income tax slab rate.

PPF, NSC, Sukanya Samriddhi, Senior Citizens Savings Scheme interest rates slashed.

Finance ministry on Wednesday has announced a cut in interest rates of small savings schemes. According to the circular by ministry dated 31 March, the interest rates of small savings schemes have been reduced by 50-100 basis points for April-June quarter of the financial year 2021-22. The interest rates for small savings schemes are reviewed and notified by the finance ministry on a quarterly basis.

From 1 April, Public Provident Fund (PPF) will get an interest rate of 6.4%. The interest for National Savings Certificate (NSC) have been reduced to 5.9%. Among other small savings scheme, the Sukanya Samriddhi Yojana will fetch the interest rate of 6.9%.

Similarly, the interest rate for the five-year Senior Citizens Savings Scheme has been lowered to 6.5%. The interest on the senior citizens' scheme is paid quarterly. The interest rate on Kisan Vikas Patra (KVP) has been cut to 6.2%.

Interest rate on post office savings deposits has been slashed to 3.5%. On the other hand, term deposits of one-five years will fetch interest rate in the range of 4.4-5.8%, to be paid quarterly, while the interest rate on five-year recurring deposit is pegged at 5.3%.

The government continues to rely on small savings for financing its fiscal deficit, say economists. "For FY22 again financing from small savings is pegged at a significant ₹3.9 lakh crore or 26% of the fiscal deficit," SBI economists had earlier said in a note.

For the April-June quarter of last year, the government had cut interest rates on small savings schemes by up to 140 basis points and since then they have remained steady. With this reduction, the interest rates of small savings schemes have been slashed by a total of 120-250 bps during the current financial year.

The finance ministry also extended the deadline for linking the Permanent Account Number (PAN) to Aadhaar by another three months."Central Government extends the last date for linking of Aadhaar number with PAN from 31st March, 2021 to 30th June, 2021, in view of the difficulties arising out of the COVID-19 pandemic," the Income Tax department tweeted.

Governments allocated $10 trillion for economic stimulus in just two months—and for some countries, their response as a percentage of GDP was nearly ten times what it was in the financial crisis of 2008–09.

The COVID-19 crisis is one of the worst health emergencies the world has witnessed for a century, and its economic impact could be just as steep. While it took several quarters for unemployment to peak in other crises, the economic shock of the COVID-19 crisis has been larger than that of any previous crisis—and it materialized within weeks. Five weeks into the crisis, the weekly number of jobs lost in the United States continues to exceed any pre-COVID-19 record. In some sectors, demand came practically to a halt in a matter of days as a result of lockdown measures.

Governments’ economic responses to the crisis is unprecedented, too: $10 trillion announced just in the first two months, which is three times more than the response to the 2008–09 financial crisis (Exhibit 1).1 Western European countries alone have allocated close to $4 trillion, an amount almost 30 times larger than today’s value of the Marshall Plan. The magnitude of government responses has put delivery into uncharted territory. Governments have included all shapes and forms in their stimulus packages: guarantees, loans, value transfers to companies and individuals, deferrals, and equity investments—as if advice from all modern schools of economic thought has been applied at the same time

AFTER MONTHS OF STALLED negotiations and partisan squabbling, Congress passed $900 billion in emergency coronavirus relief in addition to a $1.4 trillion omnibus spending bill to fund the government through late next year.

The historic legislation is the second largest stimulus in U.S. history and comes more than eight months after Congress overwhelmingly passed a $2 trillion stimulus package in late March. The federal government has now spent a total of more than $3 trillion to combat the pandemic, but since the passage of the CARES Act in the spring and the absence of more aid until now, the U.S. has seen a resurgence of the virus with a record number of cases, deaths and hospitalizations and millions more Americans falling into poverty and losing their jobs.

Topics Joe Biden | Coronavirus | Stimulus package

Topics United States | Joe Biden | Stimulus package