“I say now, as I said then, that a man should keep his little brain attic stocked with all the furniture that he is likely to use, and the rest he can put away in the lumber room of his library, where he can get it if he wants it.”- Sherlock Holmes, The Five Orange Pips.

Recently, I have been reading the book Flow by Mihaly Czikszentmihalyi. In the book I came across an extremely interesting fact. Do you know how much information a human brain can process at any given point of time?

At most we can manage seven bits of information such as sound, visual stimuli or emotion or thought at anyone time, and it takes 1/18 of a second to discriminate between one set of bits and another. Thus, it is possible to process at most 126 bits of information per second or 7560 per minute. Now just imagine you are trying to focus on a really important task. Yet your attention is divided amongst 5 other things. How well do you think you will succeed at that particular task? Given the information that you have. The answer is in all probability you will be worse off doing the task while multitasking vs focusing on just one thing at a time.

Let’s see what Charlie Munger has to say on the entire idea of Multitasking:-

“ I think people who multitask pay a huge price. They think they're being extra productive, and I think when you multitask so much you don't have time to think about anything deeply, you are giving the world an advantage you shouldn't do, and practically everybody is drifting into that mistake.”- Charlie Munger

Given that we will be worse off when it comes to completing tasks while multitasking. What do you think will happen if we multitask when it comes to different investing philosophies?

The entire purpose of why different value investors or other legendary investors have a philosophy related to investing is that they know what they are doing and do not want to drift endlessly in this game. There are thousands of ways to make money in the stock markets and if you don’t know which furniture you want in your brain attic. Then it can lead to unnecessary collection of furniture that might not be comfortable for you. After a few years of investing, finding a philosophy or a way that works for you becomes extremely important.

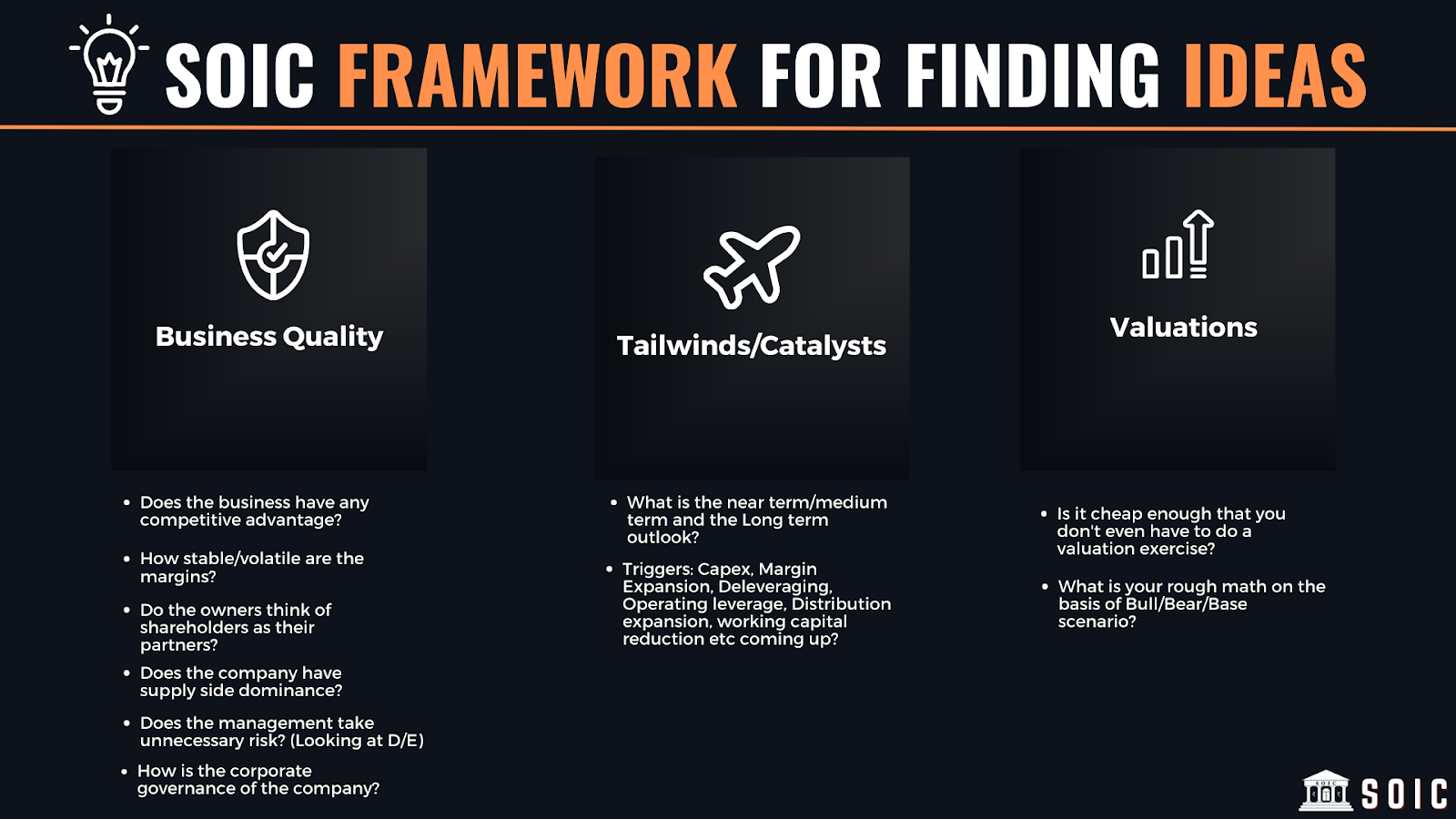

After reading about multiple philosophies over the years, I have finally made a 3 point framework which is what investing essentially boils down to:-

Business Quality: How good is the industry and the Business?

1. Does the business have any competitive advantage?

2. Is there presence of Supply Side Dominance| The Most Powerful Generator of Returns in B2B Businesses

3. How stable are the margins and the working capital cycle?

4. What about Management? (Forensic checks discussed in recent webinar)

5. Applying Michael Porter’s Five Forces framework to check for strength and weakness in the entire value chain

6. Runway for growth? Big fish in an ocean or a small fish in shallow waters?

7. Is the business scalable?

Tailwinds/Catalysts: What will lead to growth?

The Indian Market is a growth market. Finding triggers for growth are really important. Asking these 3 questions can help you identify whether growth is there or not?

1. What are the near term/medium term and long term growth triggers?

2. Why will the growth materialise? Some hints to look out for- Capacity expansion, Margin Expansion, Working capital reduction (will lead to free cash flow growth), Expansion of distribution, operating leverage, Product mix change and finally reduction in interest cost etc.

3. Classify the business into grades of cyclicality: Deeply cyclical, shallow cyclical or structural in nature?

Valuation: The Most Important Aspect

1. Is the business cheap enough that I don’t even need to do a proper valuation exercise?

2. Does it fall under the Growth at Reasonable Prices?

3. How many years do I have to look into the future to justify the valuation today?

I will discuss one of the most important aspects when it comes to assessing the quality of business. This is one of the most important mental models when it comes to long term investing and finding ideas that pass the checks of business quality in the 3 point framework:- Does the business have any Supply Side dominance?

Now you will ask, what do you mean by Supply side dominance Ishmohit?

I will first explain what is meant by demand and then I will come to the essence of supply side dominance. Understanding one will lead to a better understanding of the other.

Essentially in any business or any industry there are two things when it comes to dealing with market forces: Demand and supply. What we mean by demand, is what is the need or want for a particular product and at what pace is this need or want growing per annum?

Now just stop over here and think for a moment. Whenever, you read equity reports or any research reports. One aspect is common amongst them, most of the reports are busy in predicting the demand growth per annum for different industries or a particular segment. Some of the popular narratives for demand side are:-

1. The Auto Penetration rate in India is really low when compared to the USA and China. This is bound to grow.

2. The Per capita steel consumption in India is low when we compare it to the other countries. Thus, the per capita consumption of steel will increase.

3. The Indian chemical industry is growing at 12% per annum and will outgrow the Chinese Chemical industry when it comes to the next 3-5 years.

These are some of the common methods in which demand side factors are discussed in equity reports. Let’s look at what Benjamin Graham says:-

“Obvious prospects for physical growth in a business do not translate into obvious profits for investors.”

One of the most popular industries where the demand side has been growing perpetually is education. But how many companies can you think of that created wealth in this sector in India?

How many Passenger Vehicle companies have done well in India leaving Maruti aside over the long run?

How many aviation companies have created wealth in India?

Growth or growth in demand itself is also the ideology of a cancer cell. I am not saying that you should completely ignore demand growth and end up buying Castrol where demand is stagnant. You should pay far less attention to demand growth as analysts or the street gives. What you should really focus on is:- Supply Side Dominance.

“Go where competition is either weak or Dumb.”- Charlie Munger

Now, let’s imagine 3 scenarios. Read this slowly and try to come up with an answer yourself:-

1. There are 8 vegetable shops in an area, the demand growth is healthy. However due to intense competition amongst them. There is a pricing war. Who do you think will end up winning in such a situation?

2. There are 8 vegetable shops. However, one shop out of them has the licence to sell dragon fruit which the other shops don’t have (let's assume hypothetically). Demand is more or less growing for the Dragon Fruits. Do you think this shopkeeper will be able to charge a premium?

3. Finally, out of these 8 shops. One of the shopkeepers apart from selling vegetables also exclusively owns a shop for selling building materials in the neighbourhood. Although, the demand for building materials tends to be cyclical. Whenever, the demand booms. This shopkeeper makes a killing as he’s the only one in the neighbourhood.

In the first case, due to an intense pricing war. Most of the shopkeepers over a period of time will struggle to earn returns that will be equivalent to their cost of capital (ROCE<COC). Thus, there’s an absence of supply side dominance.

In the second case due to the presence of a licence in selling dragon fruits. The second shopkeeper will make better Economic Profits/Return on capital as compared to the other shop keepers. In this case, there is presence of supply side dominance when it comes to one division of the business.

In the last case, the shopkeeper in his building material division will do really well because he has built supply side dominance in this part. No other shopkeeper is present in this division. However, he will go through periods of disruption when demand goes down. In this case there is supply side dominance, but demand seems to be shallow cyclical and follows its own pattern.

Now lets substitute all these 3 shops and come look at 3 real life business case studies to understand more about supply side dominance:-

1. Let’s look at the example of the Indian Pharmaceuticals industry. Lupin is one of the companies that did really well in 2010-2015. Essentially, Lupin and other generic companies were selling medicines in the USA at a time when there was very little competition. Over a period of time what happened is that for a lot of these generic drugs there were multiple ANDA filers. In other words, for one copycat medicine there were 15 filers from India and secondly the distributors consolidated. Now just think about the first example of 8 shopkeepers selling the same vegetables. This is essentially what ended up happening here. Just take a look at the Return on capital employed for Lupin post 2017:-

2. Now, let’s look at the example of the Indian Maize Processing industry. Gujarat Ambuja Exports is one of the dominant companies when it comes to this segment and almost has a 25% market share which will further expand post the capacity expansions. However, this was not always the case. The company originally started as an edible oil processor. Only post 2009, the company has built its maize processing business just like the shopkeeper who was selling Dragon fruits :).

In this case, the business has grown and the competitive intensity has weakened as a lot of competitors have shut down their capacities as they took on a lot of debt. Following are the competitive advantages of GAEL:-

3. Now finally coming to the last example of a company that has supply side dominance but is going through temporary headwinds or some cyclicality in demand. Sudarshan chemicals is one of the few Organic Pigment manufacturers and has almost a 35% market share in India. On the supply side it has the largest capacity and the products that the company is making are differentiated and it’s difficult to get these products approved by the suppliers. Points to switching cost, technical know how and barriers to entry when it comes to the process. Now, this business is like the third shop we talked about that goes through headwinds and shallow cyclicality in demand. This is where the real art of investing lies:- How to differentiate between temporary and permanent headwinds. Business is dominant on the supply side. However, the Raw Material prices have increased sharply lately. Which is leading to a crunch in the margins of the company. This has led to the valuations becoming reasonable and the company is doing a 700 crores+ capex that will effectively add 1500 crores to the topline. A good company with supply dominance+Temporary headwinds is what leads to reasonable valuations. Over a period of time, if the headwinds go away and the growth comes (as in Q1FY23, entire capex goes live). Then this is like buying a lottery ticket with low downside when such situations happen. I am personally assessing this closely, as the headwinds are likely to persist for next 2-3 quarters. Waiting for some sign that headwinds will go away.

If you spend more time assessing the supply side vs the Demand side. Then you will end up improving as an investor. For instance:- Deepak Nitrite has made a quasi monopoly of domestic production of Phenol. However, its a bulk commodity. One needs to keep tracking what happens on the supply side. What if Reliance forward integrates and announces a capacity for producing Phenol? That is the type of questions you need to keep asking yourself and you need to keep looking out for such information when it comes to assessing supply side dominance.

In conclusion, I will leave you with a simple way to assess supply side dominance. Make a simple list of market leaders. Track and study those businesses, often this is where the future winners are found. An example of such a list–

Dear reader, I ask you, Which company are you invested in that has supply side dominance? Do let me know in the comment section below!

No comments:

Post a Comment