stocks climbed Thursday as markets calmed after recent banking sector turmoil. The Dow Jones Industrial Average rose 0.4 percent to 32,859.03, while the broad-based S&P 500 picked up by 0.6 percent to 4,050.83. The tech-heavy Nasdaq Composite Index jumped 0.7 percent to 12,013.47.

While investors have been wary since federal officials seized control of

Silicon Valley Bank

earlier this month -- marking the collapse of one of three midsized lenders -- there have not been more US casualties since then.

This raised hopes that the emergency steps taken by regulators and private lenders have staved off contagion.

On Thursday, Treasury Secretary

Janet Yellen

told a conference that recent events including the banking sector turmoil "remind us of the urgent need to complete unfinished business."

This includes finalizing post-crisis reforms and considering "whether deregulation may have gone too far."

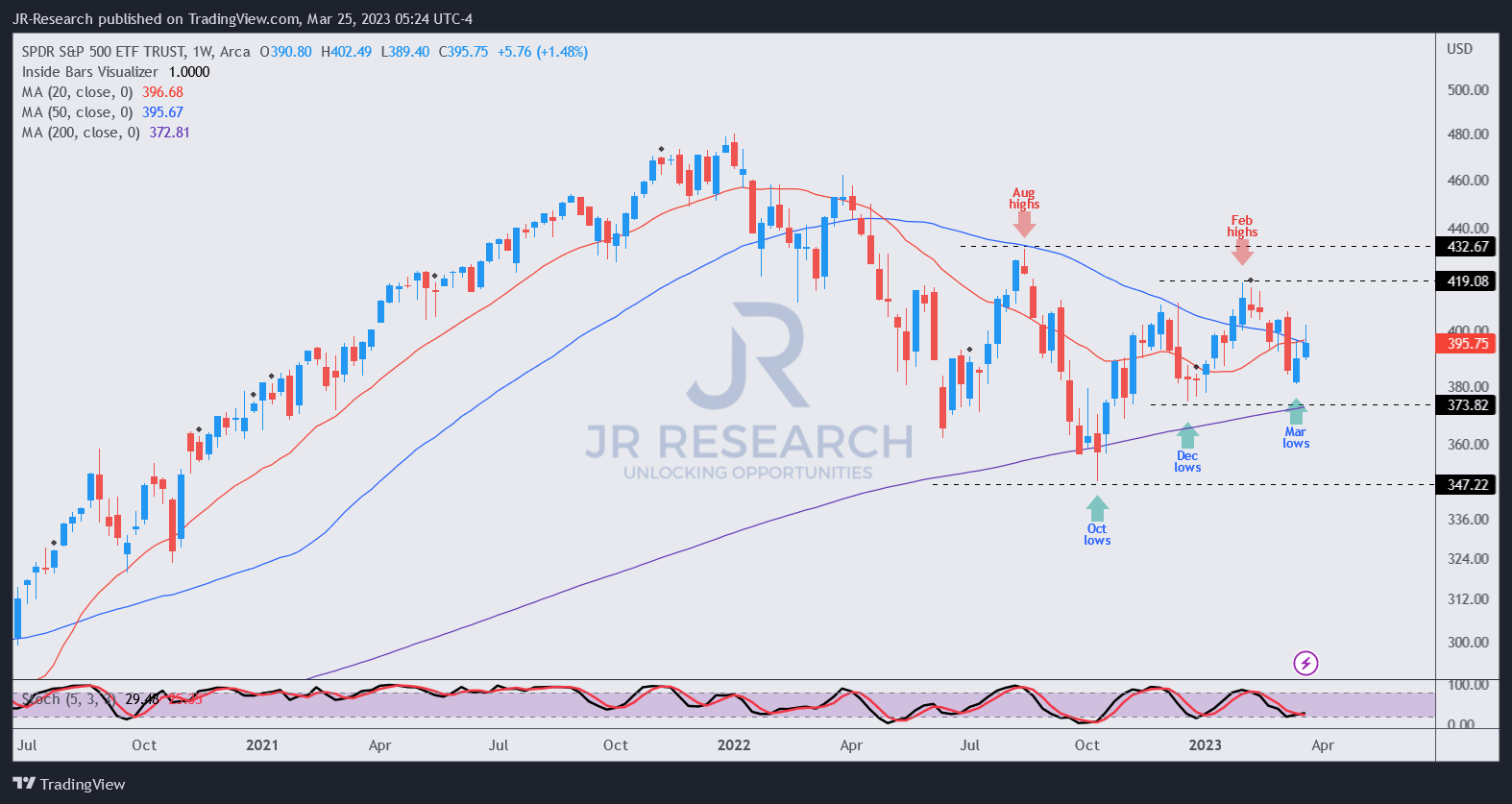

The S&P 500 ETF bottomed out two weeks ago despite the banking crisis. Risk-on sectors have lifted the gloom, as underlying sector rotations suggest bullishness.

The Fed significantly shifted its messaging by removing "ongoing" from its latest FOMC statement. As a result, it could suggest that the inflation threat is less significant than in February.

The market's concerns now are likely less focused on the inflation threat but have shifted to assessing the impact of a potentially severe economic downturn.

While there are broad risk-on factor tailwinds pushing it forward, potential contagion risks from the ongoing banking crisis could put a halt to its progress.

I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Significant developments have occurred since our last update for the S&P 500 ETF (NYSEARCA:SPY) (SPX) on March 7. The week ended with the stunning collapse of Silicon Valley Bank or SVB (SIVB) and Signature Bank (SBNY).

The speed of the bank failures caught the Fed off-guard, as Fed Chair Jerome Powell indicated in his recent post-FOMC meeting press conference. As such, the now-infamous social media bank run of SVB has given new challenges and impetus for the Fed and the US government to deliberate.

Despite that, the SPY has recovered from its March drubbing, even though it remains 5.6% from re-testing its February highs. The bearish thesis suggesting that the bank crisis may not be over is a critical risk for bullish investors to consider.

Moreover, the back-and-forth commentary by Treasury Secretary Janet Yellen has likely failed to placate investors as they parsed whether a system-wide temporary blanket guarantee of all deposits could be in the works.

Investors also had to endure a still-hawkish Fed, as it increased its Fed Funds rate by another 25 bps, bringing the target range to between 4.75% to 5%. However, the Fed's hawkish messaging has been downgraded somewhat as the FOMC changed the critical wording from its commentary: "ongoing increases in the target range will be appropriate."

Instead, the most recent statement highlighted that "some additional policy firming may be appropriate," implying that the Fed believes its assessment of the inflation threat has likely toned down markedly from its previous update.

Has the market anticipated the likely changes before last week's FOMC meeting? Yes, it did. Accordingly, the market's FFR projections no longer point to a terminal rate of 5.5% (pre-SVB collapse).

The market has dropped its FFR expectations significantly, seeing a pivot from June, with the FFR expected to fall to about 4% by the end of the year.

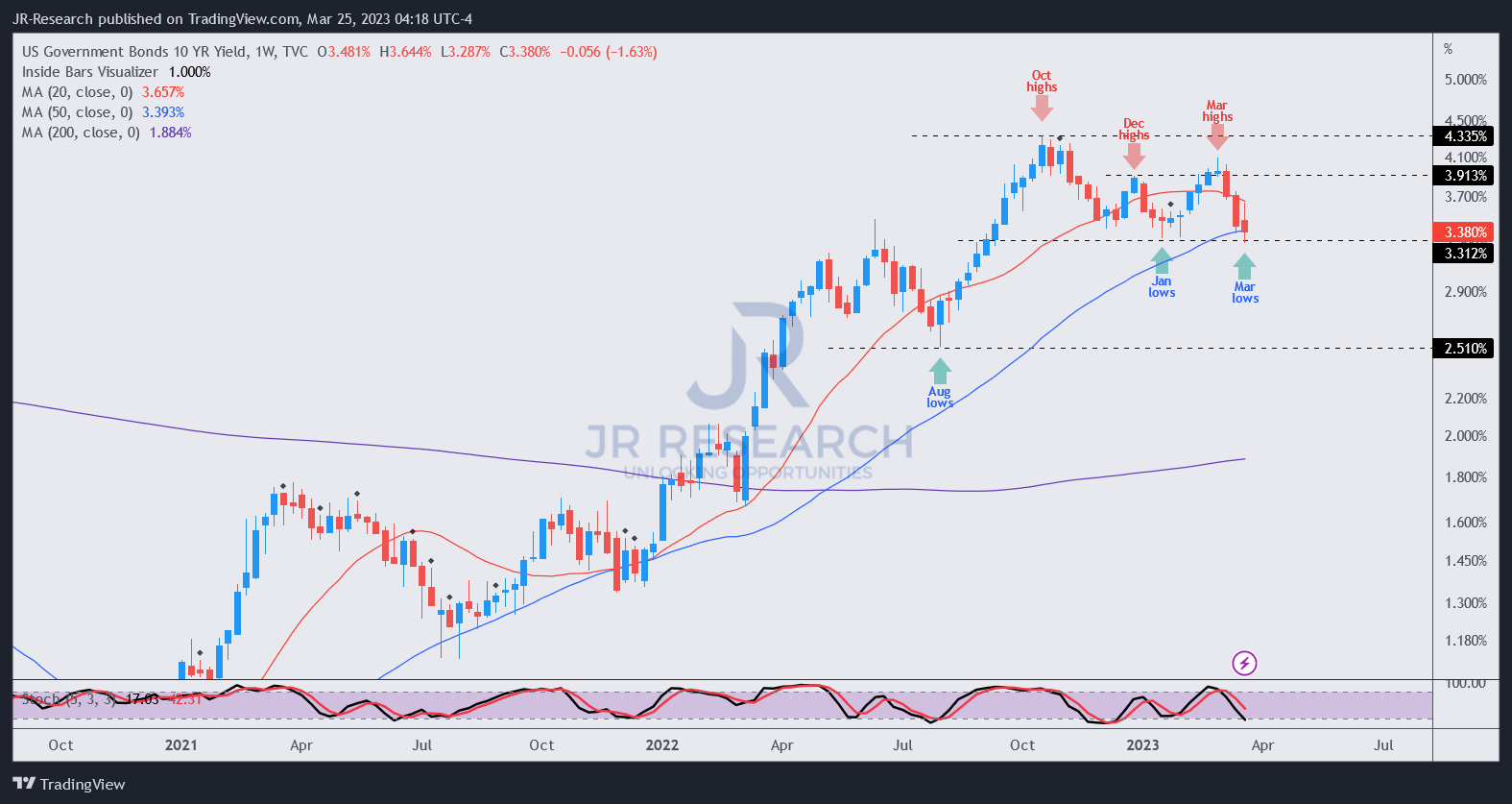

So, what do we observe from the price action on the 10Y bond yield?

US10Y yield price chart (weekly)(TradingView)

As seen above, market operators have positioned for the top in the 10Y Treasury yield at the start of March (pre-SVB collapse). It also formed a bull trap or false upside breakout against its uptrend continuation pattern.

We informed members of our service on February 14 that the price action in the US10Y suggests that a "yield-driven pullback" on the SPY could intensify, even though the SPY was still hovering around its late January highs. Moreover, we informed members to watch for a bull trap in the 10Y that could help form a bottom in the SPY.

Note that we had already downgraded our directional bias on January 30 after upgrading it in late December and taking advantage of the early January rally. It also coincided with the bottoming process of the 10Y yield in January.

The SPY then pulled back sharply toward the post-SVB collapse lows before bottoming out two weeks ago. As such, we believe watching the price action in the 10Y could provide meaningful clues to the forward developments in the SPY.

So, where are we now? The bull trap in the 10Y that we posited has played out accordingly. It has also re-tested January lows with no resolution yet.

With that in mind, how should investors consider positioning their SPY exposure from here?

Backtesting historical data from Sundial Capital suggests that:

Similar reversalsin the past have led to consistent declines in Treasury yields across most time frames. The 10-year yield tends to show a downward bias over the next two months after such a reversal, falling 75% of the time -Sundial Capital

Edward Yardeni also highlighted the following:

Inverted yield curves tend to signal peaksin the interest rate cycle, with the 2-year Treasury yield rising faster than the 10-year yield and exceeding it during the tail end of monetary policy tightening cycles. -Yardeni Research morning briefing 21 March 2023

Have we really reached a peak? Let's see.

US2Y/US10Y price chart (weekly)(TradingView)

By overlaying the 2Y yield over the 10Y yield, we can clearly observe the price action of the inversion.

The inversion topped out in early March and has flattened somewhat, moving closer to the lows in September. Still, it's too early for bond bulls to rejoice, as a decisive breakdown below September levels is necessary to suggest that March's peaks are unlikely to be retaken.

As such, the tailwind from the market's expectations of the Fed pivot has likely played its part in the recent bottoming process for the SPY. So with that in mind, what could help drive the SPY moving forward and not re-test its recent March lows?

We indicated previously that the S&P 500 has likely bottomed out in October, as we updated our members on October 21: "We have the bullish reversal condition, as anticipated."

While the SPY has not looked back since forming those lows, the threat of a full-blown recession has also risen. With the SPX trading at an NTM adjusted P/E of about 17.5x, it's not configured for a deeper recession, even at its October lows. We expect the SPX to fall back to levels between 2,600 and 2,900 in a full-blown recession.

However, since the market is forward-looking, market operators will likely bring us to those levels first, even before a severe recession could be felt.

What could bring us there? If the banking crisis spreads further, significantly crimping lending and worsening credit availability, the contagion could spread to other critical sectors of the economy.

An important area that regional banks have focused on is the commercial lending space. However, by the time you read this article, savvy hedge funds have already placed their bets accordingly.

Bloomberg reported that "almost 40% of sharesin the iShares U.S. Real Estate ETF (IYR) are sold short,the highest proportion since June." Notably, regional banks accounted for "80% of bank lending to commercial properties."

While US regulators emphasized that the "overall financial systemis still sound," bank deposits flowed out of smaller banks at the highest levels over the past year.

Accordingly,smaller banksrecorded a deposit decline of $120B, while the largest 25 institutions saw a deposit growth of about $67B.

Hence, the stress in the financial system has likely not been resolved. Investors shouldn't ignore the possibility of a "Black Swan" event, as full ramifications from the Fed's record rate hikes could break more things.

SPY price chart (weekly)(TradingView)

Even though the SPY finished markedly above last week's lows, the momentum failed at a critical juncture, rejected by the 50-week moving average or MA (blue line).

Risk-on sectors like Consumer Discretionary (XLY), Tech (XLK), and Communications (XLC) have lifted the gloom over SPY.

In contrast, value sectors like Energy (XLE) have underperformed significantly. In addition, defensive sectors like Consumer Staples (XLP), Healthcare (XLV), and Utilities (XLU) have also underperformed their risk-on peers since December.

As such, it's pretty clear risk-on factors have driven the SPY since its December lows, which demonstrated the underlying sector rotations under the hood.

It suggests why market operators have turned bullish broadly and, therefore, could potentially bring us closer to the end of the bear market than investors think.

With the SPY at a critical juncture, we believe the reward/risk is balanced now, factoring in higher risks of a deeper recession that we need to discount.

As such, we are moving to the sidelines from here and will watch how the market operators are positioning over the next few weeks for clarity.

Pakistan inflation soars to 47%, Onions up 228% and wheat up 120%

Pakistan is struggling with a significant shortage of foreign exchange to sustain its balance of payments due to the ongoing economic crisis and IMF loan delay.

Crisis-hit Pakistan recorded a new high in inflation based on sensitive price indicator (SPI) as it went to around 47% year on year (YoY) the week ended March 22, 2023, according to Pakistan Bureau of Statistics (PBS) data. This came following a continued hike in prices of essential commodities.

The report also stated that the country's foreign exchange reserves have risen to $10.14 billion as of the week ending on March 17, 2023.

Currently, Pakistan is struggling with a significant shortage of foreign exchange to sustain its balance of payments due to the ongoing economic crisis and IMF loan delay.

Both have been negotiating since early February on an agreement that would release USD 1.1 billion to the cash-strapped, nuclear-armed country of 220 million people, and it's supercritical for the liquidity-challenged country.

Stephanie Pomboy expects US stocks to plunge 30% and a broad economic downturn to take hold.

Consumers, businesses, and real estate developers are being hit by soaring interest rates, she said.

Prepare for stocks to crash and the American economy to suffer a sweeping downturn that rivals the Great Recession, Stephanie Pomboy has warned.

"The everything bubble has now burst, and that's going to hit everything, everywhere all at once," the Macro Mavens founder told Fox Business on Wednesday. "There's a lot of ugly stuff coming down the pike."

The stock market could plunge 30%, and the current pressure on banks could spread to commercial real estate, corporate credit, municipal bonds, and other markets, Pomboy said.

The economist noted that debt levels are higher today than before the mid-2000s housing crash, and the Federal Reserve has dramatically raised interest rates over the past year. The upshot is that consumers are struggling to afford their car loans and credit cards, and many companies and real estate developers are feeling the squeeze, she continued.

"This is really like 2007, 2008 all over again," Pomboy said. "Except I think it's going to devolve even faster than it did then because of the speed and magnitude of the Fed's rate hikes."

Pomboy, who worked at ISI for over a decade before starting her own investment-research firm in 2002, castigated the US central bank. She accused it of repeatedly pumping too much money into the economy, boosting asset prices to unsustainable highs, then ratcheting up interest rates and causing painful crashes.

"The Fed basically has us ping-ponging from asset bubble to bust," she said. "It's lather, rinse, repeat."

Fed Chair Jerome Powell and his colleagues hiked rates by another 25 basis points on Wednesday. Since last March, they've raised them from virtually zero to upward of 4.75% — the highest level since 2007.

If asset prices tumble and the economy weakens, the Fed could reverse course and rapidly cut rates in the months ahead, Pomboy said.

Pomboy is one of several experts sounding the alarm on stocks and the economy. Jeremy Grantham, a market historian and veteran investor, expects the S&P 500 to plummet 50% and a painful recession to take hold.

The Federal Reserve announced it hiked interest rates by another 25 basis points, in line with Wall Street's predictions.

This marks the central bank's ninth hike since it began raising rates March 2022, as well as its first announcement following the recent fallout in the banking sector. The increase takes the benchmark federal funds rate to a target range between 4.75%-5%.

Most officials now expect the policy rate to peak at 5-5.25 per cent this year and for that level to be maintained until at least 2024. Policymakers pencilled in a series of rate cuts by the end of next year, with the federal funds rate falling back down to 4.3 per cent.

The US central bank last published officials’ estimates in December, when most expected the federal funds rate to peak at 5-5.25 per cent.

In the days leading up to the March meeting, former officials, economists and investors were at odds over how the Fed should proceed, with those in favour of a pause arguing that the central bank could further unsettle an already tenuous situation by ploughing ahead with another rate rise.

Following the collapse of SVB and Signature, the Fed rolled out an emergency lending facility to help small and medium-sized banks struggling with a flight of depositors to larger institutions. It also worked with the Treasury department and the Federal Deposit Insurance Corporation to guarantee deposits held at the two failed banks — even those above the $250,000 threshold for government insurance.

On Tuesday, Treasury secretary Janet Yellen said US authorities could take further steps to shore up the financial system if necessary.

Her comments followed an announcement on Sunday from the Fed and five other leading central banks that they would move to improve access to US dollar liquidity after the forced takeover of Credit Suisse by UBS brokered by Swiss officials last weekend.

The Fed has come under fire over the recent string of bank failures, facing questions about how closely officials were monitoring regional lenders following a roll-back in the rules governing them -- measures that Powell himself endorsed in 2019.

Economies In Trouble: Argentina, Lebanon, UK, New Zealand On The Hot Seat

Inflation in Argentina crossed the 100% mark, UK faces a tough cost-of-living crisis – many more such examples are prevalent as the world faces a mammoth economic crisis

Pakistan News | Inflation In Pakistan | Pakistan Economic Crisis | News18 Exclusive | News18Price rise and rising inflation is forcing Pakistanis from lower strata of the society to end their lives. Two reports have surfaced showing the effects of the economic crisis on the lives of Pakistani people.A report from Pakistan’s Surjani surfaced where an unemployed man poisoned his wife and two little daughters by poisoning their drinking water and also attempted to end his own life due to unemployment and failing to meet the needs of his family.

A 'perfect storm' of recession, debt, and out-of-control inflation is coming for markets this year, 'Dr. Doom' Nouriel Roubini says

A recession, debt crisis, and stagflation trifecta is going to strike the US economy this year, according to Nouriel Roubini.

Roubini, known for his doomsayer predictions on Wall Street, has warned for months that another financial crisis will hit markets.

A "perfect storm" is brewing in 2023, and a markets are going to get hit with a recession, debt crisis, and out-of-control inflation, according to "Dr. Doom" economist Nouriel Roubini.

Roubini, one of the first economists to call the 2008 recession, has been warning for months of a stagflationary debt crisis, which combines the worst aspects of 70s-style stagflation and the '08 debt crisis.

"I do believe that a stagflationary crisis is going to emerge this year," Roubini said in an interview with Australia's ABC on Thursday.

With consumer inflation still sticky at 6.4%, Roubini estimated that the Federal Reserve would need to lift benchmark rates "well above" 6% for inflation to fall back to its 2% target.

But that could spark a severe recession, stock market crash, and an explosion in debt defaults, leaving the Fed with no choice but to back off its inflation fight and let prices spiral out of control, he added. The result would be a steep recession anyway, followed by more debt and inflation problems.

"Now we're facing the perfect storm: inflation, stagflation, recession, and a potential debt crisis," Roubini warned.

He has remained ultra-bearish on the economy, despite the market's growing hope that the US could skirt a recession this year.

Though more bullish commentators are making the case for a healthy rebound in the S&P 500, which fell 20% last year, Roubini has previously warned the benchmark stock index could slide another 30% as investors battle extreme macro conditions.

"They will continue to go down," he said of stocks, pointing to the recent sell-off as investors price in higher interest rates from the Fed. "The market is already correcting."

Brace for the S&P 500 to plunge 50% and a painful recession to strike as the 'everything bubble' bursts, elite investor Jeremy Grantham warns

Jeremy Grantham expects stocks to plunge and a recession to hit as the "everything bubble" bursts.

The investor warns the S&P 500 could halve in value to around 2,000 points in a worst-case scenario.

Jeremy Grantham has warned the implosion of an "everything bubble" could tank the S&P 500 by up to 50%, and plunge the US economy into a painful recession.

The prices of stocks, bonds, real estate, fine art, and other investments ballooned to unsustainable highs during the pandemic, Grantham said. The market historian and GMO cofounder shared his thesis with economist David Rosenberg during a recent Rosenberg Research webcast.

The current bubble is "pretty damn big" compared to previous ones, and dwarfs the dot-com boom in scope, Grantham said.

"It's bad enough just doing the equity market in 2000," he said. "This time, we have done a dead ringer for the equity market, plus the gravy, we've done the housing market and the bond market."

"Be advised this is not a genteel setback like 2000," Grantham continued, predicting a bear market could persist until deep into next year. He noted the dot-com crash only caused a mild recession, but even so, the Nasdaq index plummeted 82% and the S&P 500 halved in value during that period.

FRANKFURT, March 16 (Reuters) - The European Central Bank raised interest rates as promised by 50 basis points on Thursday, sticking with its fight against inflation and facing down calls by some investors to hold back on policy tightening until turmoil in the banking sector eases.

A rout in global markets triggered by last week's collapse of Silicon Valley Bank (SVB) and made worse by doubts around the future of Switzerland's Credit Suisse had prompted some to question whether the ECB would pause its rate-hiking cycle.

Yet in line with its often-repeated guidance, the central bank for the 20 countries that share the euro lifted its deposit rate to 3% - the highest level since late 2008 - as inflation is seen overshooting its 2% target through 2025.

Lagarde said the ECB decision was adopted by "a very large majority" of its policy-makers.

Reuters Graphics Reuters Graphics

Bank shares had been in freefall this week, spooked first by SVB's collapse, then a plunge in the value of Credit Suisse, a lender that has long been dogged by problems.

But the Swiss National Bank threw Credit Suisse a $54 billion lifeline overnight, a big enough show of force to send its shares back up around 20% and lift other bank stocks.

Three sources close to the Governing Council told Reuters it was the SNB's move that had given ECB policymakers confidence to press ahead with the 50 basis point rate increase.

The key worry for the ECB is that monetary policy works via the banking system, and a full blown financial crisis would make its policy ineffective.

That left the ECB in a dilemma, pitting its inflation-fighting mandate against the need to maintain financial stability in the face of overwhelmingly imported turmoil.

ECB Vice-President Luis de Guindos said euro zone exposure to Credit Suisse was "quite limited" and Lagarde noted that in any case, the policy tools the ECB had at its disposal meant there was no trade-off between financial and price stability.

Inflation, the bank's primary responsibility, is far higher than in previous crises and the ECB's new projections, published on Thursday, put price growth above its 2% target through 2025, an overriding concern for many of its policymakers.

Inflation is seen averaging 5.3% this year, 2.9% in 2024 and 2.1% in 2025, the ECB said, adding that these projections were finalised before the current turmoil.

Lagarde noted the bank was starting to see signs that its policy tightening was having an impact on the economy, notably through credit channels.

India CPI inflation in February drops to 6.44%, higher than Street estimates

India's retail inflation for February decreased to to 6.44 percent in February as against 6.52 percent in January 2023, according to data published by the Ministry of Statistics and Programme Implementation on March 13.

While the CPI in January stood at 6.52 percent, the same for December 2022 was at 5.72 percent. In November, it was 5.88 percent and 5.59 percent in October 2022.

Payrolls rose 311,000 in February, more than expected, showing solid growth

POINTS

Nonfarm payrolls rose by 311,000 in February, above the 225,000 Dow Jones estimate.

The unemployment rate increased to 3.6%, above expectations.

Average hourly earnings climbed 4.6% from a year ago, less than expected, in a positive sign for inflation.

Leisure and hospitality, retail, and government led job creation by sector.

Job creation decelerated in February but was still stronger than expected despite the Federal Reserve’s efforts to slow the economy and bring down inflation.

Nonfarm payrolls rose by 311,000 for the month, the Labor Department reported Friday. That was above the 225,000 Dow Jones estimate and a sign that the employment market is still hot.

The unemployment rate rose to 3.6%, above the expectation for 3.4%, amid a tick higher in the labor force participation rate to 62.5%, its highest level since March 2020.

The survey of households, which the Bureau of Labor Statistics uses to compute the unemployment rate, showed a smaller 177,000 increase. A more encompassing unemployment measure that includes discouraged workers and those holding part-time jobs for economic reasons rose to 6.8%, an increase of 0.2 percentage point.

There also was some good news on the inflation side, as average hourly earnings climbed 4.6% from a year ago, below the estimate for 4.8%. The monthly increase of 0.2% also was below the 0.4% estimate.

Though the jobs number was stronger than expectations, February’s growth represented a deceleration from an unusually strong January. The year opened with a nonfarm payrolls gain of 504,000, a total that was revised down only slightly from the initially reported 517,000. December’s total also was taken down slightly, to 239,000, a decrease of 21,000 from the previous estimate.

Stocks were mixed after the release, while Treasury yields were mostly lower.

“Mixed is an apt descriptor. There’s something for everybody in there,” said Liz Ann Sonders, chief investment strategist at Charles Schwab. “We’re still in a recession for certain parts of the economy.”

The jobs report likely keeps the Fed on track on raise interest rates when it meets again March 21-22. But traders priced in less of a chance that the central bank will accelerate to a 0.5 percentage point increase, dropping the likelihood to 48.4%, or about a coin flip, according to a CME Group estimate.

“Perhaps the best news from this report was the easing of wage pressures,” said John Lynch, chief investment officer at Comerica Wealth Management. “A drop in the largest costs for businesses is a welcome development. Nonetheless, 50 basis points is still on the table for the March policy meeting, given recent economic strength and dependent on next week’s [consumer price index] report.”

Leisure and hospitality led employment gains, with an increase of 105,000, about in line with the six-month average of 91,000. Retail saw a gain of 50,000. Government added 46,000, and professional and business services saw an increase of 45,000.