Summary

- The S&P 500 ETF bottomed out two weeks ago despite the banking crisis. Risk-on sectors have lifted the gloom, as underlying sector rotations suggest bullishness.

- The Fed significantly shifted its messaging by removing "ongoing" from its latest FOMC statement. As a result, it could suggest that the inflation threat is less significant than in February.

- The market's concerns now are likely less focused on the inflation threat but have shifted to assessing the impact of a potentially severe economic downturn.

- While there are broad risk-on factor tailwinds pushing it forward, potential contagion risks from the ongoing banking crisis could put a halt to its progress.

- I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Significant developments have occurred since our last update for the S&P 500 ETF (NYSEARCA:SPY) (SPX) on March 7. The week ended with the stunning collapse of Silicon Valley Bank or SVB (SIVB) and Signature Bank (SBNY).

The speed of the bank failures caught the Fed off-guard, as Fed Chair Jerome Powell indicated in his recent post-FOMC meeting press conference. As such, the now-infamous social media bank run of SVB has given new challenges and impetus for the Fed and the US government to deliberate.

Despite that, the SPY has recovered from its March drubbing, even though it remains 5.6% from re-testing its February highs. The bearish thesis suggesting that the bank crisis may not be over is a critical risk for bullish investors to consider.

Moreover, the back-and-forth commentary by Treasury Secretary Janet Yellen has likely failed to placate investors as they parsed whether a system-wide temporary blanket guarantee of all deposits could be in the works.

Investors also had to endure a still-hawkish Fed, as it increased its Fed Funds rate by another 25 bps, bringing the target range to between 4.75% to 5%. However, the Fed's hawkish messaging has been downgraded somewhat as the FOMC changed the critical wording from its commentary: "ongoing increases in the target range will be appropriate."

Instead, the most recent statement highlighted that "some additional policy firming may be appropriate," implying that the Fed believes its assessment of the inflation threat has likely toned down markedly from its previous update.

Has the market anticipated the likely changes before last week's FOMC meeting? Yes, it did. Accordingly, the market's FFR projections no longer point to a terminal rate of 5.5% (pre-SVB collapse).

The market has dropped its FFR expectations significantly, seeing a pivot from June, with the FFR expected to fall to about 4% by the end of the year.

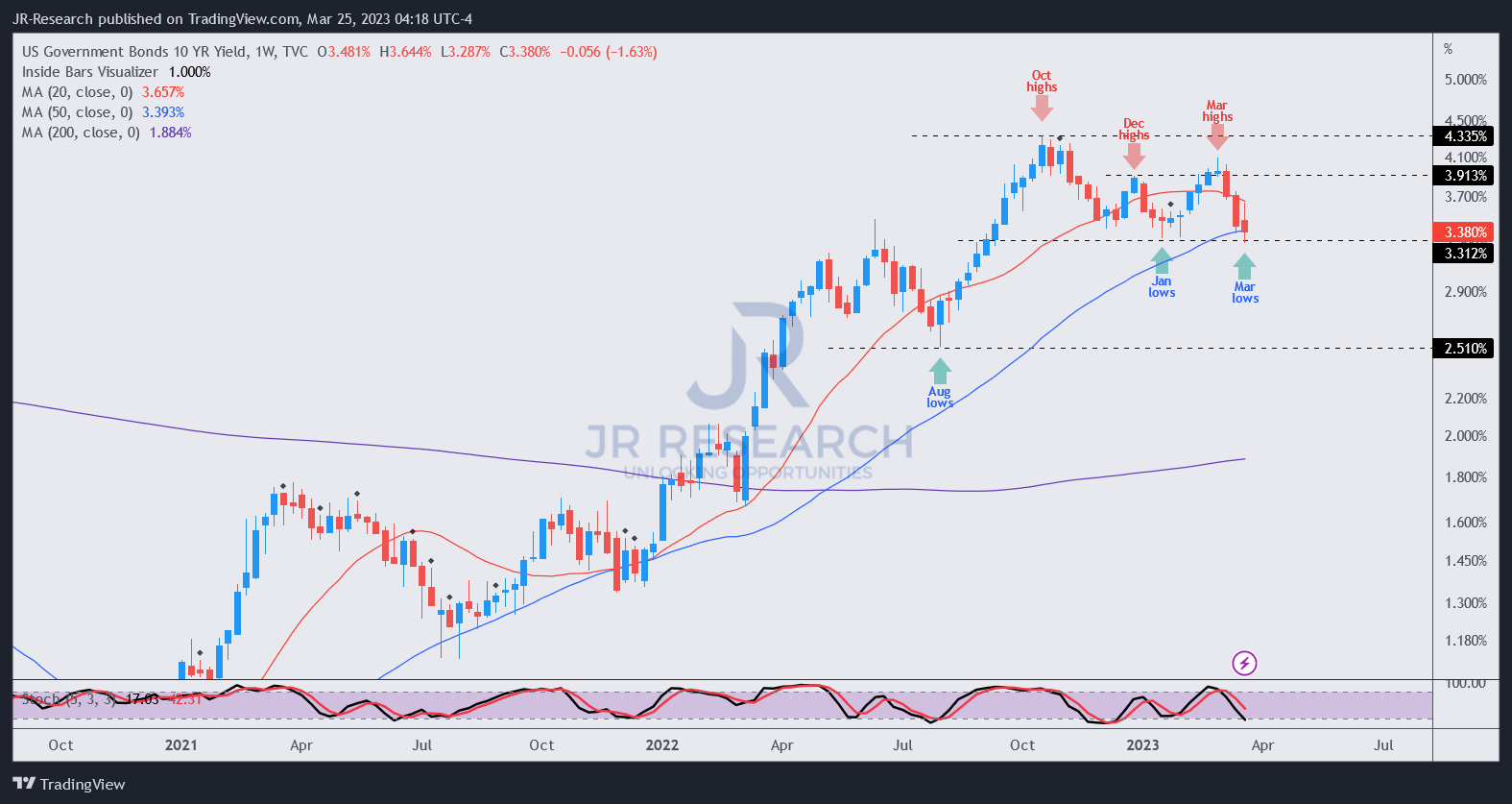

So, what do we observe from the price action on the 10Y bond yield?

US10Y yield price chart (weekly) (TradingView)

As seen above, market operators have positioned for the top in the 10Y Treasury yield at the start of March (pre-SVB collapse). It also formed a bull trap or false upside breakout against its uptrend continuation pattern.

We informed members of our service on February 14 that the price action in the US10Y suggests that a "yield-driven pullback" on the SPY could intensify, even though the SPY was still hovering around its late January highs. Moreover, we informed members to watch for a bull trap in the 10Y that could help form a bottom in the SPY.

Note that we had already downgraded our directional bias on January 30 after upgrading it in late December and taking advantage of the early January rally. It also coincided with the bottoming process of the 10Y yield in January.

The SPY then pulled back sharply toward the post-SVB collapse lows before bottoming out two weeks ago. As such, we believe watching the price action in the 10Y could provide meaningful clues to the forward developments in the SPY.

So, where are we now? The bull trap in the 10Y that we posited has played out accordingly. It has also re-tested January lows with no resolution yet.

With that in mind, how should investors consider positioning their SPY exposure from here?

Backtesting historical data from Sundial Capital suggests that:

Similar reversals in the past have led to consistent declines in Treasury yields across most time frames. The 10-year yield tends to show a downward bias over the next two months after such a reversal, falling 75% of the time - Sundial Capital

Edward Yardeni also highlighted the following:

Inverted yield curves tend to signal peaks in the interest rate cycle, with the 2-year Treasury yield rising faster than the 10-year yield and exceeding it during the tail end of monetary policy tightening cycles. - Yardeni Research morning briefing 21 March 2023

Have we really reached a peak? Let's see.

US2Y/US10Y price chart (weekly) (TradingView)

By overlaying the 2Y yield over the 10Y yield, we can clearly observe the price action of the inversion.

The inversion topped out in early March and has flattened somewhat, moving closer to the lows in September. Still, it's too early for bond bulls to rejoice, as a decisive breakdown below September levels is necessary to suggest that March's peaks are unlikely to be retaken.

As such, the tailwind from the market's expectations of the Fed pivot has likely played its part in the recent bottoming process for the SPY. So with that in mind, what could help drive the SPY moving forward and not re-test its recent March lows?

We indicated previously that the S&P 500 has likely bottomed out in October, as we updated our members on October 21: "We have the bullish reversal condition, as anticipated."

While the SPY has not looked back since forming those lows, the threat of a full-blown recession has also risen. With the SPX trading at an NTM adjusted P/E of about 17.5x, it's not configured for a deeper recession, even at its October lows. We expect the SPX to fall back to levels between 2,600 and 2,900 in a full-blown recession.

However, since the market is forward-looking, market operators will likely bring us to those levels first, even before a severe recession could be felt.

What could bring us there? If the banking crisis spreads further, significantly crimping lending and worsening credit availability, the contagion could spread to other critical sectors of the economy.

An important area that regional banks have focused on is the commercial lending space. However, by the time you read this article, savvy hedge funds have already placed their bets accordingly.

Bloomberg reported that "almost 40% of shares in the iShares U.S. Real Estate ETF (IYR) are sold short, the highest proportion since June." Notably, regional banks accounted for "80% of bank lending to commercial properties."

While US regulators emphasized that the "overall financial system is still sound," bank deposits flowed out of smaller banks at the highest levels over the past year.

Accordingly, smaller banks recorded a deposit decline of $120B, while the largest 25 institutions saw a deposit growth of about $67B.

Hence, the stress in the financial system has likely not been resolved. Investors shouldn't ignore the possibility of a "Black Swan" event, as full ramifications from the Fed's record rate hikes could break more things.

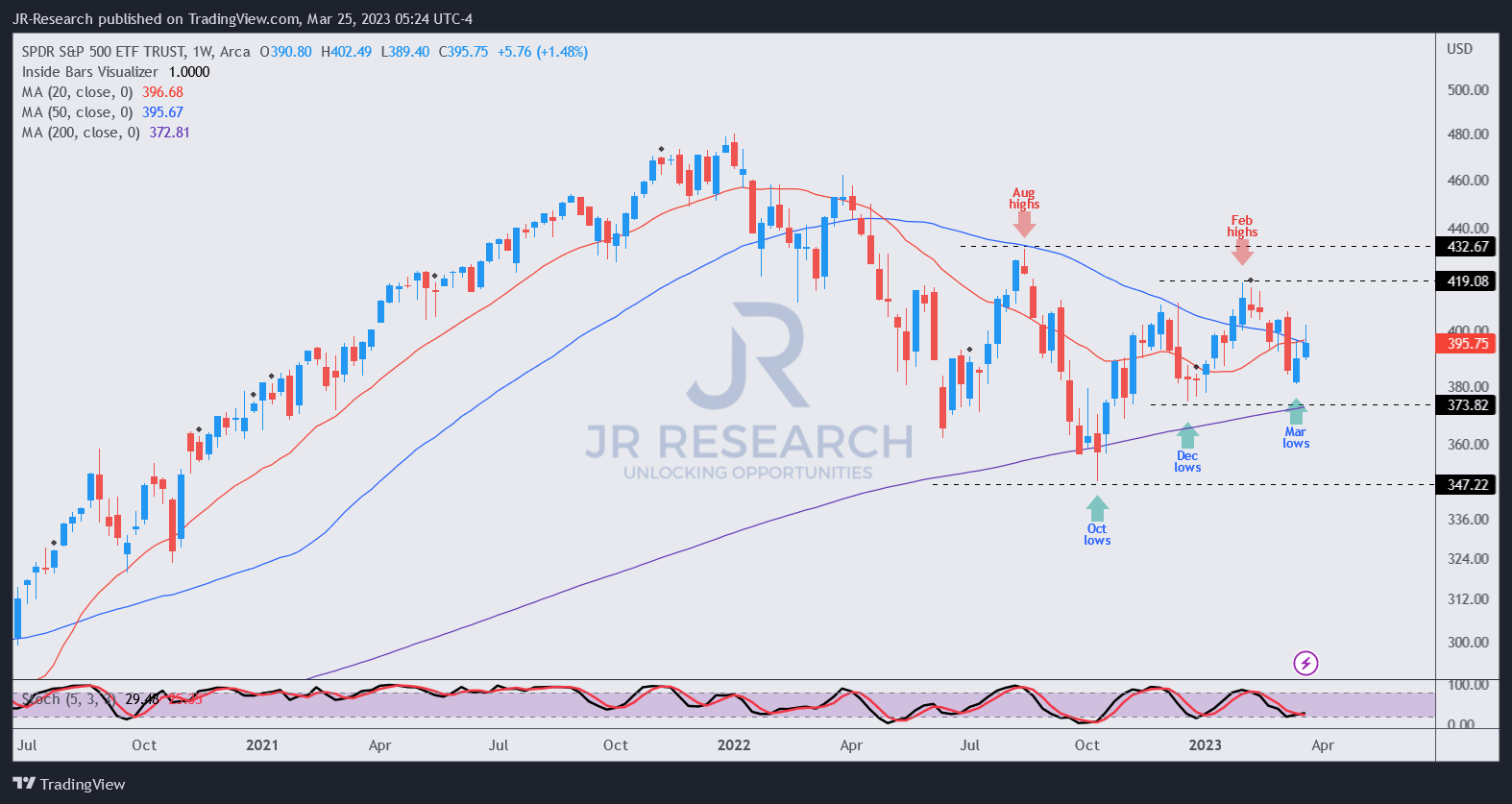

SPY price chart (weekly) (TradingView)

Even though the SPY finished markedly above last week's lows, the momentum failed at a critical juncture, rejected by the 50-week moving average or MA (blue line).

Risk-on sectors like Consumer Discretionary (XLY), Tech (XLK), and Communications (XLC) have lifted the gloom over SPY.

In contrast, value sectors like Energy (XLE) have underperformed significantly. In addition, defensive sectors like Consumer Staples (XLP), Healthcare (XLV), and Utilities (XLU) have also underperformed their risk-on peers since December.

As such, it's pretty clear risk-on factors have driven the SPY since its December lows, which demonstrated the underlying sector rotations under the hood.

It suggests why market operators have turned bullish broadly and, therefore, could potentially bring us closer to the end of the bear market than investors think.

With the SPY at a critical juncture, we believe the reward/risk is balanced now, factoring in higher risks of a deeper recession that we need to discount.

As such, we are moving to the sidelines from here and will watch how the market operators are positioning over the next few weeks for clarity.

No comments:

Post a Comment