Why your returns are less than your fund's...and how to bridge the gap

Many investors complain that while the funds they own have healthy trailing returns, their actual returns are subpar. We investigate why

Over the last decade or so, equity mutual funds have emerged as a powerful investment option. A look at the 10-year returns of the various categories of funds proves this point. The 10-year category average returns (as of November 2019) of open-ended multi-cap, mid-cap and smallcap funds stand at 11.46, 14.08, 12.04 per cent, respectively, handsomely beating the fixed-income options. This has resulted in rising assets as well. In November 2009, open-ended equity-fund assets stood at 1.4 lakh crore. In November 2019, they were at 7.99 lakh crore, an annualised growth of 19.02 per cent.

SIPs have also taken off in line with the growth in fund assets. Equity investors now understand that in order to beat market volatility, they have to spread their investments over time. The SIP data from AMFI for the last three years paints a rosy picture. From about `3,000 crore in April 2016, monthly SIP flows have grown to about `8,000 crore in November 2019.

There is no dearth of success stories based on equity-fund investments as well. Over the last couple of years, in our 'How I Did It' section, we have profiled investors who have built wealth with equity funds. Yet there are many who have been left out. Such people comprise those who haven't yet started investing in equity and those who have been investing in equity but haven't been able to generate good returns.

For the latter category, the reason for mediocre returns could be wrong choice of funds or investment behaviour. If you invested in poorly performing funds, your return experience was also unsavoury. For instance, among multi-cap funds, over 10 years, the best-performing fund returned 17.52 per cent. But the worst-performing one returned just 7.48. This fact also suggests that a long-term horizon in equity is best complemented by a good underlying investment.

Many investors complain that while the funds they own have healthy trailing returns, their actual returns are subpar. The reason for this discrepancy lies in investor behaviour. It's general investment wisdom now that one should not try to time the market. However, in order to maximise their outcomes, many investors indulge in just that. By investing more at the peak and withdrawing when the market is falling, they end up doing just the opposite of what is optimal. These oscillations between greed and fear are a major cause of investor failure. These prevent an investor from getting the same returns as those given by the fund.

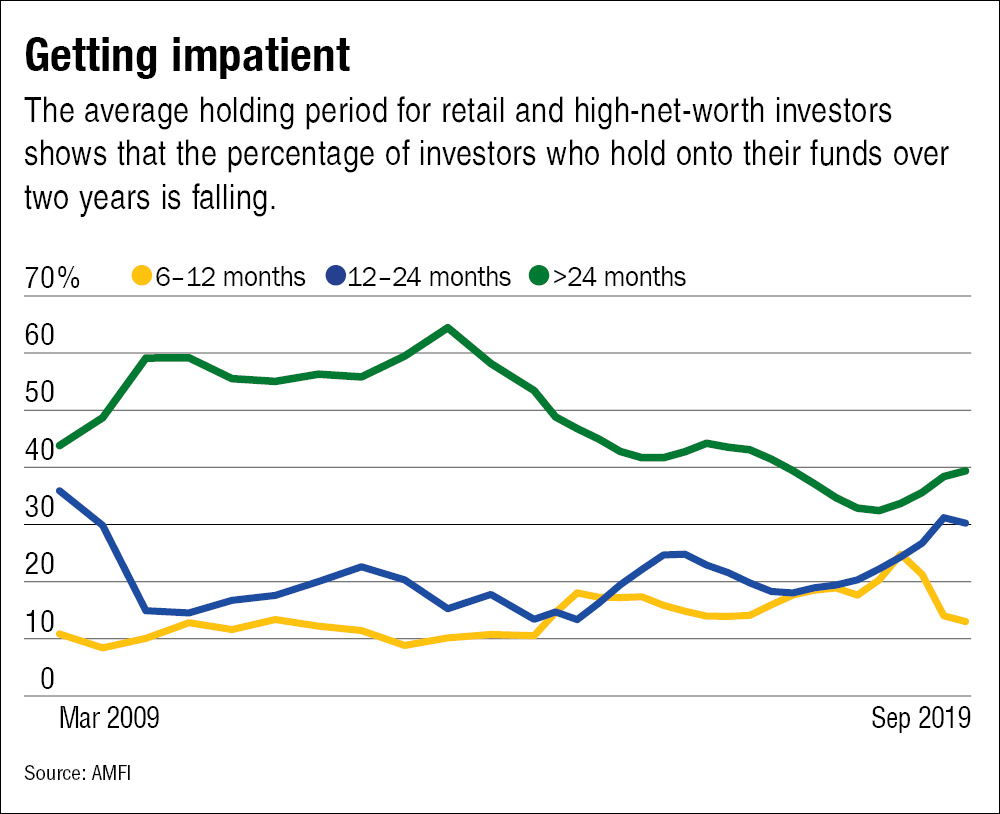

AMFI's 10-year data for the average holding period of equity funds by retail investors (including high-net-worth ones) shows a remarkable fall in the over-24-months category (see the graph 'Getting impatient'). This shows the diminishing investment horizon for retail equity investors. Given this, it's not surprising that many equity investors complain of a sub-optimal equity experience.

A gross mismatch

In order to illustrate how timing the market hurts your overall returns and why investors' returns tend to be less than actual returns, we conducted a study. Across various equity-fund categories, we considered the funds that have a 10-year history as of November 2019. In order to find the returns that an investor would have got (please note that these won't be the trailing returns because the investor would have made investments and withdrawals in the interim), we found out the internal rate of return based on indicative inflows and outflows

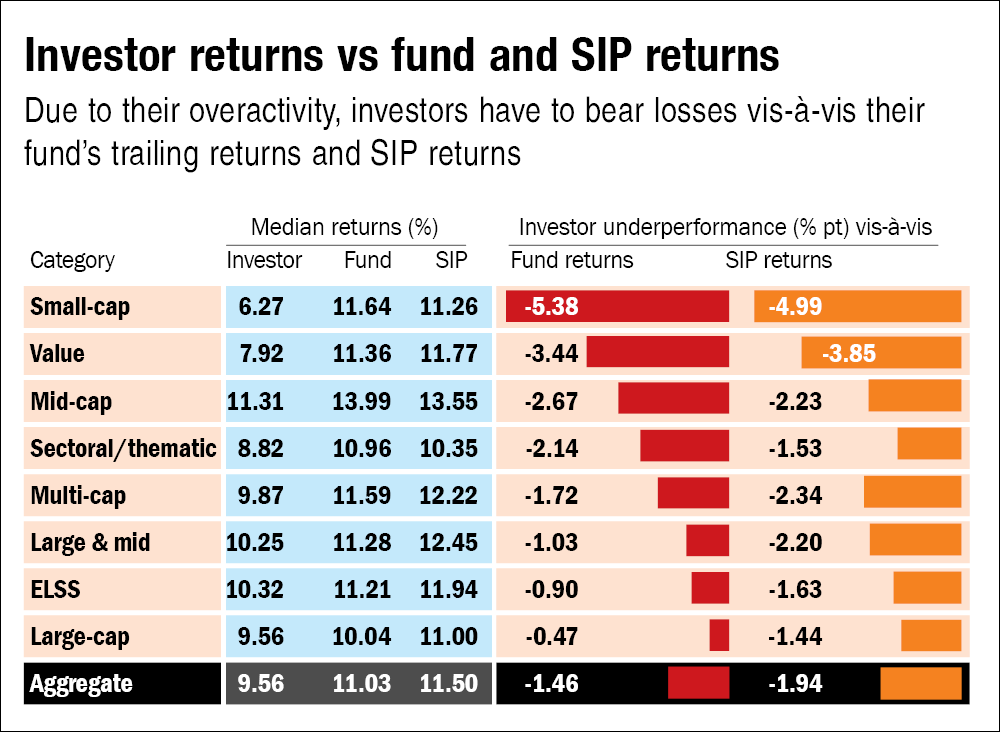

The table 'Investor returns vs fund and SIP returns' lists the internal rates of return of various fund categories against their trailing returns and SIP returns.

The table above illustrates how timing your entry and exit can cost you. On an aggregate level, the median outperformance of fund returns over investors' actual returns is 1.46 percentage points per year. This difference is least for large-cap funds (0.47 percentage points) and most for small-cap funds (5.38 percentage points). The latter number is quite understandable as, thanks to their volatility, small-cap funds do see quite erratic flows depending on where the market is headed.

However, the SIP data provides comfort. The median outperformance of SIP returns over investors' actual returns stands at a healthy 1.94 percentage points every year. For small-cap funds, this outperformance is about 5 percentage points, again suggesting that SIPs are the best way to invest in this volatile category.

Inside the investors' mind

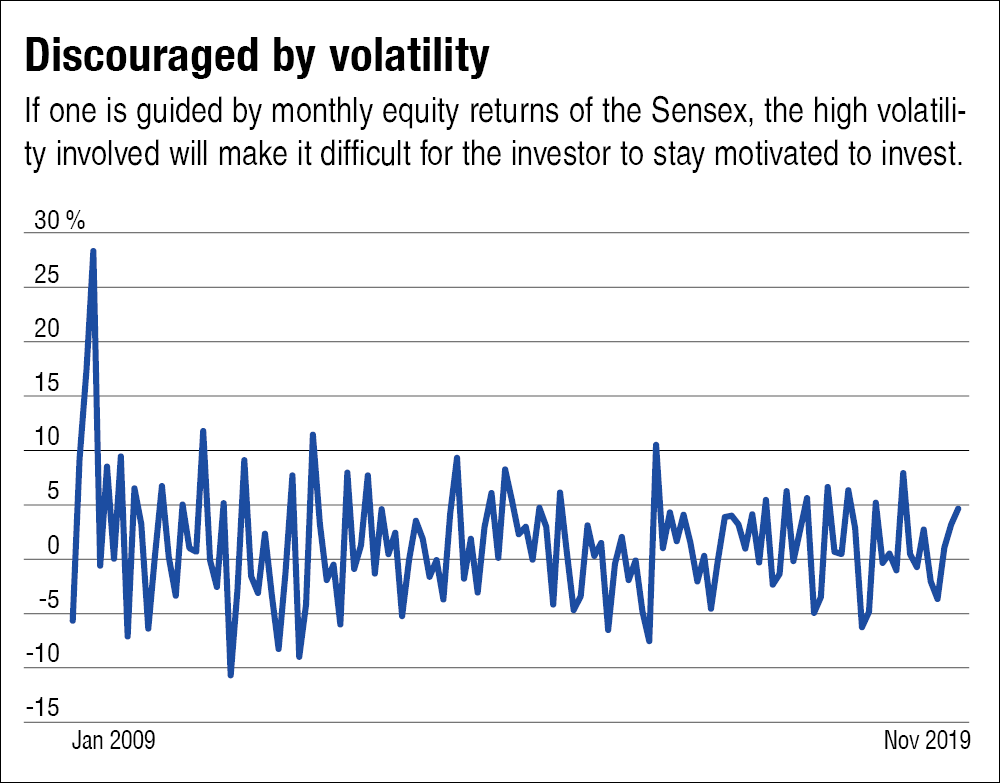

In spite of knowing that timing the market is counterproductive, why do investors still do it? Market volatility is no. 1 culprit. Investors have a tough time digesting volatility. As the graph 'Discouraged by volatility' shows, monthly Sensex returns over 10 years are a series of zigzags. Those who want dramatic returns from equity are usually disappointed by these. This causes them to cut and run. However, if the Sensex is seen every five years, this volatility dies out and a clean uptrend is visible. Indeed, the cliche 'Time in the market is more important than timing the market' prevails.

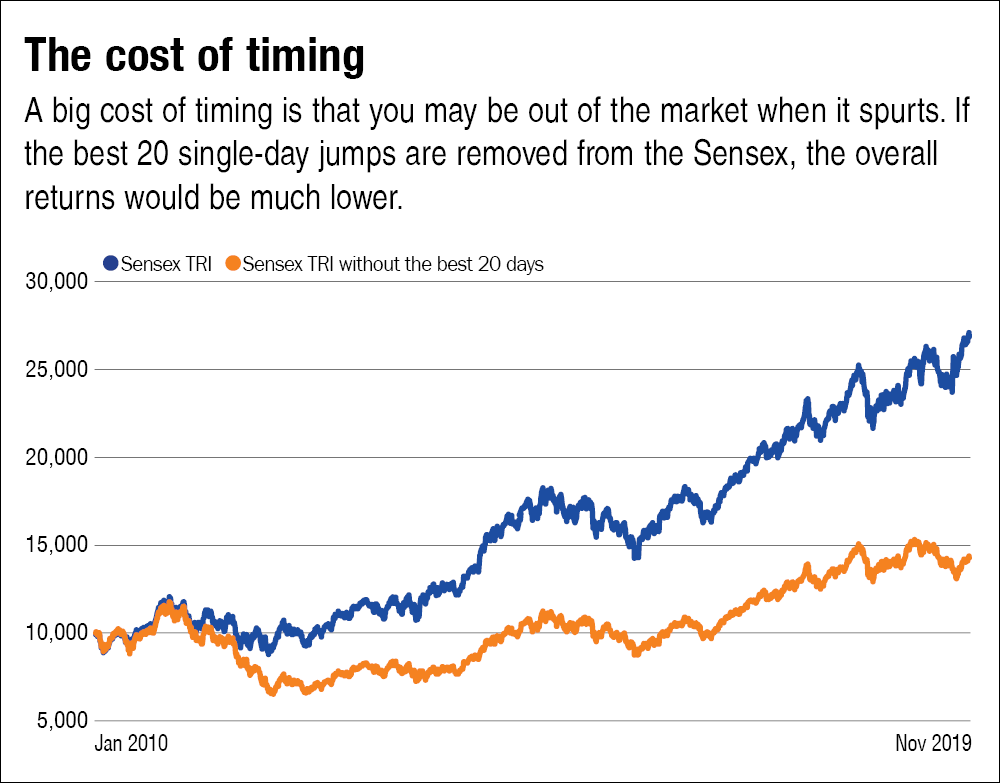

The second reason for the difference between investors' actual returns and funds' returns is that investors tend to be out of the market during crucial phases. Equity returns don't accumulate like debt returns; instead, they come in fits and starts. You may have a long phase of a downturn or stagnation, but then all of a sudden the market rebounds. If you are sitting out of the market during these rebounds, your overall returns suffer. The graph 'The cost of timing' shows investors were actually exiting the market when it soared suddenly.

Keeping it simple

Charlie Munger said, "You don't make money when you buy a stock, you don't make money when you sell a stock, you make money by being patient and you make money by waiting." Optimising your fund returns is no rocket science. From the analysis above, we can conclude that timing the market and overactivity are both harmful to your returns. Better stay invested for the long term. Second, go for SIPs. They are the best antidote to market volatility.

No comments:

Post a Comment