Inflation has reduced Rs. one lakh to just Rs. 6000 in 40 years!

The cost inflation index for the financial year 2021-2022 was recently announced. We compile 40 years of cost inflation index data to understand the devastating consequences of inflation and why our singular focus should be on beating inflation for our long term goals.

The cost inflation index (CII) is not a measure of true price inflation in India – in fact, no such metric released by the govt is. The CII is used to inflate the purchase price of taxed assets under long-term capital gains with indexation.

Therfore the CII is an approximate measure of the decrease in value of our networth with the express understanding that the actual decrease in value would be much higher. This is because many services like healthcare and education are unregulated and have much higher inflation. In addition, due to the availability of new products and services, new expenses get added up.

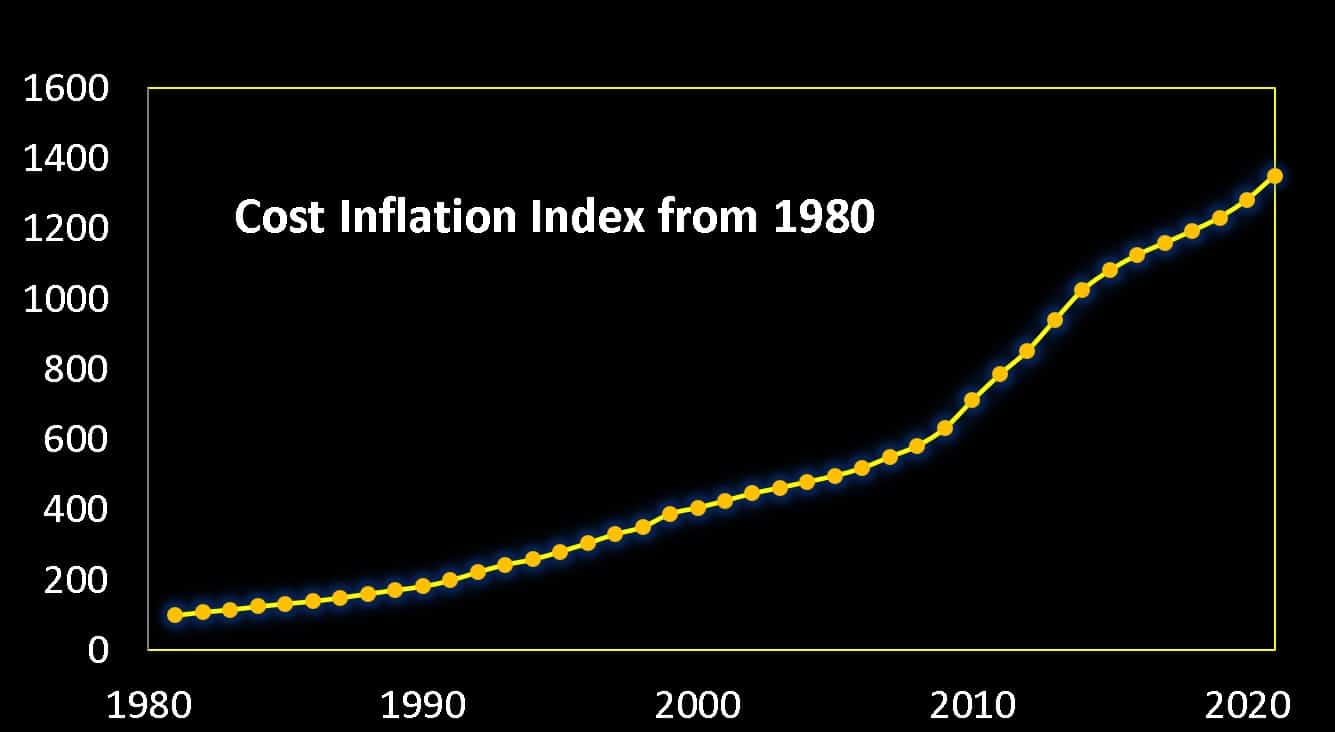

The CII initially had the base year of 1981-1982 with a value of 100. The govt then changed the base year to 2001-02. Both datasets are available here: Cost Inflation Index in India from 1980 to current financial year. We shall use the combined dataset (40 years: 1981-82 to 2021-2022) for this study.

In the 40 years that have elapsed, the CII has increased from 100 to 1351 (this is in the combined scale and will not match the latest CII date). This can be stated in many ways. Some readers tend to prefer this version:

Something that was priced Rs. 100 in 1981 will now cost at least Rs. 1351

This is, of course, the literal meaning of inflation = price increase. I prefer to focus on the effect of inflation on purchasing power. This is well conveyed by the Tamil word for inflation: பணவீக்கம் (or literally money becoming weaker).

A purchasing power of Rs. 100 in 1981 (which was significant) has been reduced to just Rs. 6 today (which is unworthy of even almsgiving).

The two statements are completely identical, but I prefer the latter as it is a bit more dramatic, highlighting the risk of chasing safety in investments. And one can add zeros to the above statement to get “Rs. one lakh has reduced to just Rs. 6000 over 40 years”.

It is important to remind ourselves that the actual inflation we face can be much higher, even for a frugal existence. Here is an example: Inflation in India: Some Real Numbers

This is the growth of the cost inflation index over the last 40 years.

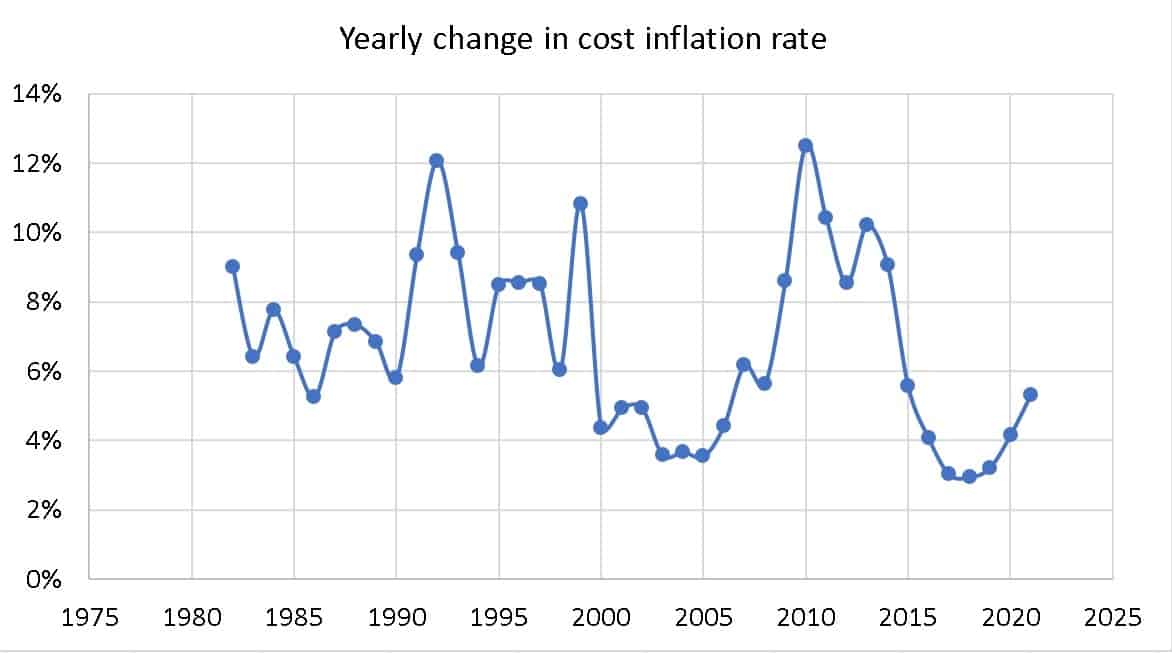

These are the annual rates of inflation. Though there is a downward slant in the rates, cost inflation could rapidly increase from time to time.

Since 2018, the 5Y cost inflation rate has been less than 5%. Have your essential expenses over the last 3-4 years been only at that level? Even in the unlikely event of this being true, it will not last long as this too is cyclic in nature.

As discussed in this video, if we do not safeguard our investment by taking adequate risks to try and beat inflation when young, we may not even buy a roadside chai in the future.

How to protect our money?

Yes, we need to invest in equity when young to combat inflation. However, this alone is not enough! Long-term investing in equity will not always be successful. See for example: What return can I expect from a Nifty 50 SIP over the next 10 years?

- We need a plan to increase our income. See, for example, Passive income is a crucial part of your retirement plan: How to get started.

- In particular, we need to manage risk systematically and craft the right variable asset allocation plan, which would help us meet our future goal no matter what the market conditions.

- We need to stick to the plan; increase investments as much as possible each year, manage risk systematically in a goal-based manner each year.

A higher income, the right investments, and active risk management is the only way to protect inflation degrading the future value of our networth.

No comments:

Post a Comment