What to do if the market crashes: Experienced investors

Top investing mistakes that experienced investors make, how to avoid them and what to do instead

Prateek is in his late 30s and has been investing for over 15 years now. He is now accustomed to the ups and downs of the market and has been investing in several funds through SIPs. He also has some investments in stocks. Like most people of his age, he also has dependents and has been saving for their future and his retirement. But Prateek is still unsure about the amount required for his goals and retirement.

Several investors face this issue. Since this is the most critical stage of the investment journey for investors, one should remember the following things.

Not saving enough: While most of the people in this age group tend to invest, they often have no idea about the amount that they should invest on a regular basis so that they can meet their goals. Thus, even though these investors are disciplined with their investments, they fail to accumulate the required corpus.

The first and foremost requirement is to set your goals. Determine your various goals, the amount you would need for them and the time horizon. While planning, one should factor in inflation as well.

Moreover, you should keep increasing your SIP amount in proportion to the increase in your income so that you can accumulate a considerable corpus.

Diversification: Most investors who have a sizable investment portfolio tend to put all their eggs in one basket or invest in several funds.

An ideal portfolio should have not more than four-five funds. The core of your portfolio should be made up of one-two diversified flexi-cap funds. Apart from that, you can invest in ELSS funds to save taxes.

Mid- and small-cap funds can help provide an edge to your returns. However, since these funds are very risky, they should not comprise more than 20-25 per cent of your entire portfolio.

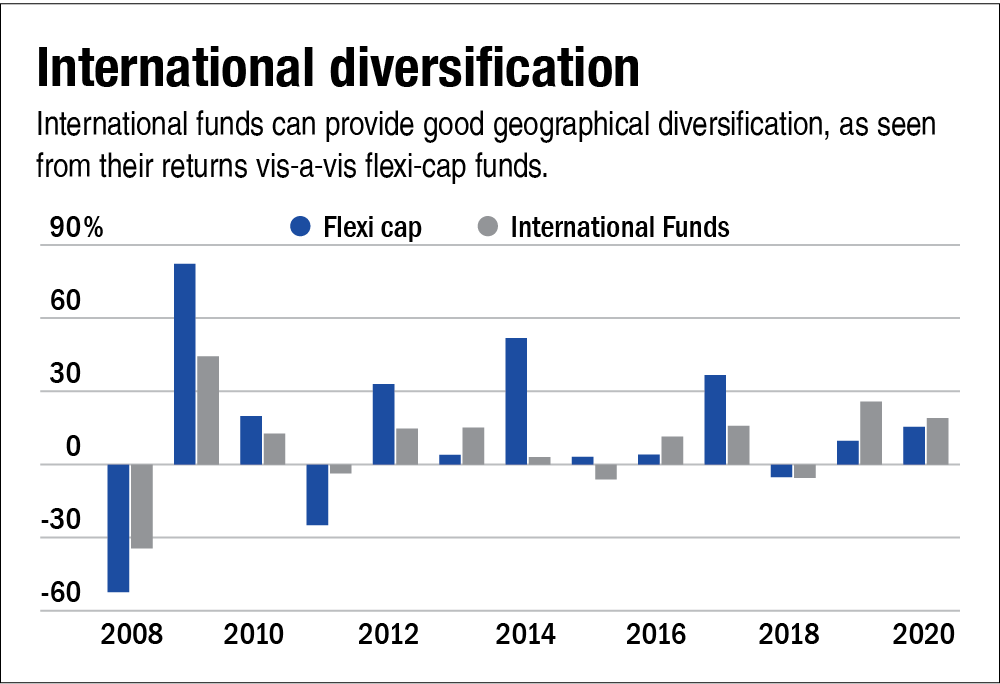

You can also add international funds, as they tend to provide geographical diversification to your portfolio (see the graph: 'International diversification')

Exiting in haste: Since these investors have been investing in the market for a long time, several of their investments seem to be giving decent returns. Therefore, they often tend to lock their profits. This is more so in the case of a runaway market where investors get lured by the returns and book profits in anticipation of an impending market correction.

No one can time the market consistently over the long term. You should exit your investments only if you need the money or if your fund has been underperforming. If your fund is underperforming, you should assess whether the entire category has been struggling or it is just your fund. If your fund is underperforming as compared to its peers, then wait for a few months to see any signs of revival. If not, then you should exit your fund. But you should keep in mind the exit load and the taxes.

Venturing into direct equity without much knowledge: While direct equity can be more rewarding than mutual funds, it is far riskier. For investors who do not have the time and knowledge to do research on companies and businesses, venturing into equity can prove to be dangerous.

You should invest in stocks if you can do research on companies before investing.

Those who lack the knowledge should go with mutual funds.

No comments:

Post a Comment