RBI may take cues from US Fed, policy stance to remain accommodative'

Rising US inflation, accompanied by tapering of the bond buying program, may reduce the extra ordinary flows into the Emerging Markets while normal flows from long term investors like pension funds may still continue.

Source: Reuters

After the recent FOMC (Federal Open Market Committee) meeting, the US Federal Reserve has moved up its target from 2024 to 2023 for the first hike in interest rates, which is a potential rate hike in future faster-than-expected. Two hikes in 2023 are the estimate. In fact, a significant number of the FOMC members, though not the majority, expect that there could be hikes as early as 2022. This is the first indication from the Fed that the current accommodative stance may continue for a while, but based on the growth-inflation numbers, there could be modifications to the policy. This converts most market participants to be expectant of possible rate changes in the coming FOMC meetings.

Rising Growth and Inflation

These broad hints from the Fed come after strong numbers both in growth and inflation. US first quarter GDP growth was at 6.40 percent as against the expectations of 6.50 percent, but a major surge in the economic activity after the pandemic battered the economy. It was Q2 of 2020 which saw the biggest fall in US growth, as it plunged by 31.40 percent. There has been an all-around improvement ever since that time. Consumers account for almost 68 percent of the economy, and their spending rose by 10.70 percent in the last quarter, compared with a 2.30 percent rise in the previous quarter. The spends on goods increased 23.60 percent, and on services, the expenditure increased by 4.60 percent.

What is behind the surge in the economy is the fiscal stimulus packages and the resultant spending. The first fiscal stimulus package was to the tune of $2 trillion of which $1.20 trillion was direct cash payments. The second introduced by Joe Biden is $1.90 trillion. These two packages put together and the direct cash which the eligible public got is quite a large amount of money which has helped aggregate demand to rise over the last few months. What is more ambitious is the new infrastructure plan, which amounts to $2 trillion. These massive spends are going to take the US economy to a new era of growth and rising demand, employment, and output.

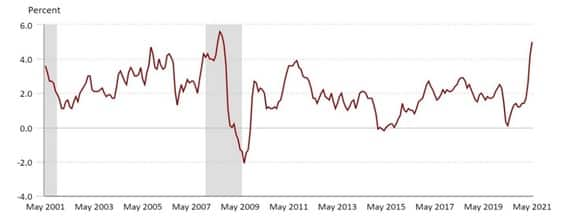

The government will collect higher corporate taxes, which is likely to be revised upwards from 21 percent to 28 percent and utilize the same for the projects. There is a clear accent on the demand side as far as counter cyclical policies are concerned, and they are more likely to bear fruits faster. The policy anchoring in the US is an average inflation of 2 percent, and the latest retail inflation number is at 5 percent. Studies of the US economy and markets have found evidence to the fact that only an inflation higher than 3 percent and rising can start denting growth.

US CPI Inflation

Source: U.S. Bureau of Labor Statistics Consequences

Rising interest rates in the US could pull down the prices of commodities especially gold in the immediate term. With the currency yield expected to move up gradually, the US unit may gain against major currencies. This may limit the rise in commodity prices. But it is important to note that any sustained rise in prices or inflation would rekindle the demand for gold. Retail inflation is a kind of a global problem now with many economies facing a surge in prices due to high oil prices or due to rise in demand post the pandemic. Under such circumstances when rates may rise in the US it will not be possible for domestic interest rates to move down, and in any case, local rates are expected to be stable to higher at the long end of the curve.

The Fed moves may influence RBI's approach to interest rate policy though it may not alter the basic commitment to an accommodative stance. However, such conditions or developments may result in the RBI gradually withdrawing the liquidity in the system. Rising US inflation, accompanied by tapering of the bond buying program, may reduce the extraordinary flows into the Emerging Markets while normal flows from long term investors like pension funds may still continue. While faster growth will endow corporates with higher sales and revenues, sustained high inflation generally reduces the purchasing power and prompts people to spend less or postpone spending.

No comments:

Post a Comment